Why we can’t fund moonshots

Failed moonshots stick out. Why can’t we find, fund, and support moonshots better?

Written by Evan Armstrong

Illustrations by Alex Merto

In 1496, Cardinal Raffaello Riario of San Giorgio purchased a statue named The Sleeping Cupid from art dealer Baldassare del Milanese. Milanese promised that this statue was an aged work of ancient antiquity. The only issue was that this was a blatant lie. The statue had actually been sculpted earlier that year by an unknown 21-year-old by the name of Michelangelo. Yes, the Michelangelo of the Sistine Chapel, of the David statue, got his start in art with a lie. He had crafted the statue by copying another artist’s style and then aging it with an acidic earth.

When the Cardinal discovered the deceit, he demanded his money back from the dealer. He would’ve been well within his rights to prosecute young Michelangelo. Instead, he recognized that talent inherent in the fabrication and insisted on becoming the artist’s first patron. Michelangelo went on to be — well, he went on to be Michelangelo.

A little bit of overenthusiastic chest-thumping isn’t the end of the world. All moonshots — atmosphere-escaping, science-pushing, mind-expanding, technology companies — are fiction at the start. They are a fool’s hope, a reality-distorting belief that world-changing progress is imminent and probable. In the startup game, you could argue that fraud is just truth’s hand called too early.

But these fibs create an inherent tension. The promises a startup makes in its early stages to investors despite having no evidence it can deliver (fun fraud) are very different from the false results it might be pressured to give to investors and consumers later down the line (incriminating fraud). The role that early-stage investors play is to be able to determine which of these two “frauds” is actually being committed.

This latest technology cycle has highlighted that tension more than ever before. Theranos exposed thousands to faulty health information, WeWork was an office building of cards, and FTX appears to have misused user funds for their hedge fund. It’s not that we haven’t seen any moonshots come to fruition in recent times. Miracles like Moderna’s COVID vaccine, SpaceX’s reusable rockets, and OpenAI’s artificial intelligence have scaled rapidly and made a widespread impact on the world during the same bull run.

And, to be fair, failure is part of the startup game. Many great companies, run by ethical people, just haven’t worked out. When investors give a startup capital, they are funding a series of experiments to determine whether a company can be successful. Sometimes, those experiments result in failure. That’s alright and to be expected.

And yet, the failed moonshots stick out. They rattle around in our narratives of startup history, make it easy to reject any big new ideas, and — without many successes to look to — keep the business models of moonshots opaque. These failures have left behind a difficult question in their wake: Why can’t we find, fund, and support moonshots better?

~

Capital is a heat-seeking missile looking for the most attractive return in the least risky ways. Even though venture capital could be funding moonshots, it often isn’t.

VC math is well known: The average VC invests in 20 companies per fund. Within that 20, roughly two will end up being smashing successes. The rest will typically go to zero. VC strategy is built around grand slams with huge returns, not base hits.

Most importantly, grand slams can be found in software. A software startup is, of course, hard and risky, but it is exponentially easier than trying to create some sort of scientific advancement. At this point, the path to building a $1B B2B SaaS startup is a playbook that is well understood and documented. Customers give you a bunch of cash up front and you don’t have to recognize that revenue for months. The gross margins will be over 80% and the free cash flow is almost always positive. It’s an appealing magnet for anyone looking for a grand slam.

Compare that to building something world-changing and unprecedented like an anti-aging startup. A startup like that will not have a clear business model, will experience significant regulatory hurdles, and — most crucially— will actually need to invent the thing. Why would a VC choose to fund a moonshot when investing in B2B SaaS is a much easier path to 3X cash-on-cash returns?

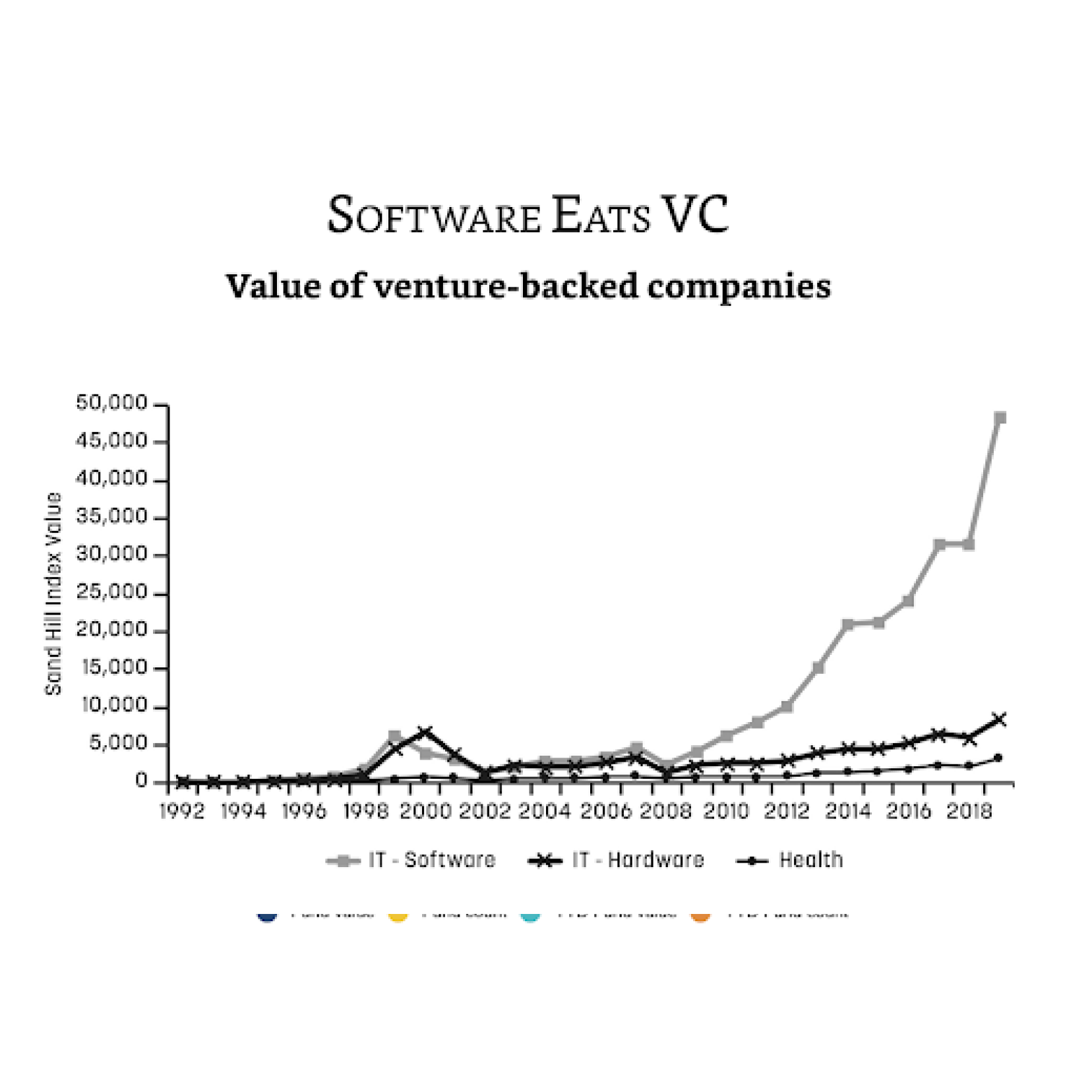

Source: The Power Law: Venture Capital and the Making of the New Future

It is a reasonable argument that there are only two types of startups: SaaS and everyone else. This has played out in the numbers: Between 1992 and 2018, investing in software has yielded far more returns than investing in hardware or health.

To get VCs to invest in moonshots you have to show stratospheric results. And because even moonshot startups are evaluated relative to the risk/return profile of software, founders of non-SaaS startups will always be tempted to fraud their way to these results.

~

But what happens when investors do show interest in moonshots? At first glance, there seems to be many reasons why their bets have failed. In the case of Theranos, the investors were neither healthcare VCs nor blue-chip funds. Even though WeWork was backed by more notable funds, including Benchmark, the primary sinner was the Softbank Vision Fund, which kept pumping money into the cash-burning extravagance of Adam Neumann. And in the case of FTX, basically every single fund on God’s green earth invested but none of them took a board seat. So many funds were interested that competition drove away the ability of investors to ask for governance rights. All of FTX’s fraud could’ve been prevented with a little oversight.

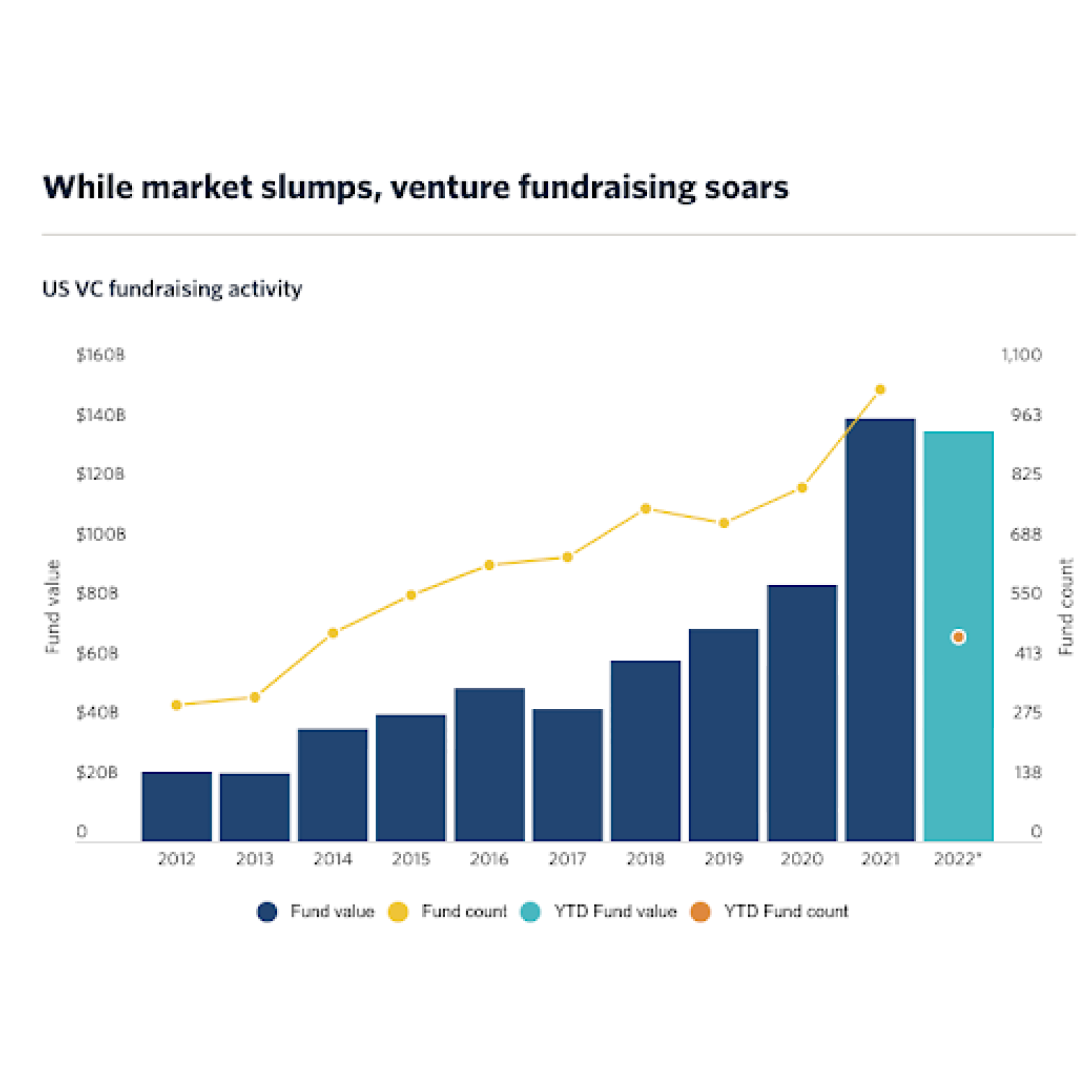

Source: Pitchbook

Though these reasons might sound disparate, they actually share a root cause. Just like how people offered to buy townhomes without ever stepping inside them in the 2021 housing market, an overabundance of capital did the same thing in startup land. There has been far too much money flowing into the sector, influenced by low-interest rates since 2008, which dramatically decreased the cost of capital. Naturally, LPs flocked to the technology sector. In 2021, more funds were raised and the fund sizes were the largest we’ve ever seen.

That meant bets were cheaper than ever and diligence fell to the wayside. Because great outcomes are so statistically rare, if a company demonstrated sufficient growth, investors were not incentivized to not look closely. That might have been ok in areas where a VC knew the rules of a game — a fund that specializes in a certain sector may be able to rely more on instinct for deals in their wheelhouse — but for large generalist funds it gets a lot trickier.

~

When young Steve Jobs sold his first run of 50 Apple computers, the company hadn’t even put anything together. They had no parts, no production line, no manuals. All they had was a hacky prototype that they showed off in computer club meetings. But he sold the product anyway. He went on to completely redefine our relationship with computers.

There are still some merits to moonshot fibs. Big dreams are audacious and they help companies at their earliest stages paint a picture of where they’ll be — if you just believe in them.

These fibs might even open the door for disrupters — those who would not have been conventionally allowed to do something if they followed a traditional path of safe, small promises.

It seems likely that we’re entering a cooling period within the technology sector. My guess is that many tourist funds will retreat, and VCs will become demanding of board seats and due diligence rights. And maybe there will be less blatant fraud over the next few years.

However, there is almost something spiritual about the pursuit of a new frontier. A true moonshot dramatically improves the human condition. And venture capital should not lose sight of funding these moonshots.

Perhaps the next question that needs to be answered is: What does a moonshot VC fund actually look like?